Using multiple bank accounts is the core financial strategy digital nomads rely on to protect their money, cut fees, and stay funded across borders. A single traditional bank account creates real vulnerabilities when you live internationally: frozen accounts, foreign transaction fees, and blocked ATM access can leave you stranded. The practice of spreading funds across two or three banking relationships, often called account diversification, addresses all three problems at once. This guide explains why nomads use multiple banks, how to structure those accounts, and how to manage them without adding stress to your travels.

Why nomads use multiple banks: the core financial case

The single biggest reason digital nomads maintain multiple accounts is that no one bank does everything well for an internationally mobile lifestyle. Traditional banks are built for people who live in one country, earn in one currency, and spend locally. When you cross borders regularly, that model breaks down fast.

The financial challenges that push nomads toward account diversification include:

- Foreign transaction fees. Traditional banks charge 3% foreign transaction fees on purchases abroad, plus separate ATM withdrawal fees. Over a full year of travel, those charges add up to thousands of dollars.

- Account freezes from AML checks. Anti-Money Laundering (AML) systems flag unusual international activity automatically. Accounts can be frozen without warning when a bank's algorithm detects logins or transactions from multiple countries in a short period.

- Currency conversion losses. Traditional banks use poor exchange rates and add conversion markups. A multi-currency fintech account converts at the mid-market rate, which is the fairest rate available.

- Limited global ATM access. Many traditional banks restrict international ATM withdrawals or charge per transaction. Running out of local cash in a country where cards are not widely accepted is a genuine emergency.

- Income receipt complications. Clients and employers often pay in USD or EUR. Receiving those payments into a local account in a country with a weaker currency means losing money on every transfer.

Each of these problems has a specific fix, and that fix usually involves a different type of account. That is why a single bank is rarely enough.

How does using multiple accounts reduce risk and increase flexibility?

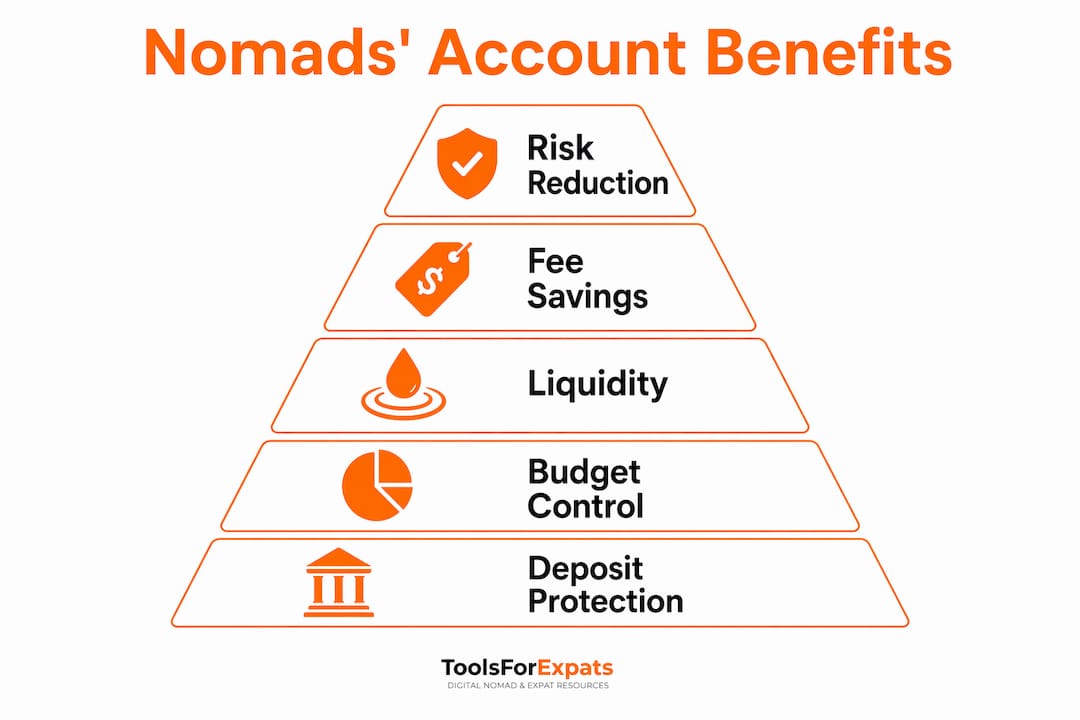

Account diversification does more than cut fees. It builds a financial safety net that keeps you funded even when one account hits a problem.

Protecting your deposits with FDIC coverage

US deposits are insured up to $250,000 per bank per depositor under FDIC rules. A nomad holding $500,000 in savings needs at least two FDIC-member banks to keep every dollar protected. That is not a niche concern. Nomads who freelance or run online businesses often accumulate significant savings before reinvesting, and deposit insurance is the simplest protection available.

Staying liquid when one account is frozen

Secondary accounts provide liquidity during compliance reviews or unexpected restrictions. If your primary account is frozen while a bank investigates international activity, a completely separate account at a different institution keeps you funded. This is not a theoretical risk. Nomads report account freezes regularly, especially after traveling through multiple countries in a single month.

Separating funds for better budgeting

Mechanical separation of funds by purpose across different accounts is one of the most underrated budgeting tools available. Keeping three months of rent in an account without a debit card means you physically cannot spend that money on impulse. This approach works better than willpower alone, and it pairs well with a structured nomad budget framework.

| Account purpose | Account type | Key benefit |

|---|---|---|

| Income receipt and savings | Home-country bank | Stability, FDIC coverage, client payments |

| Daily spending abroad | Multi-currency fintech | Low fees, mid-market rates, instant conversion |

| Long-stay local bills | Local bank account | Rent, utilities, local direct debits |

| Emergency reserve | Separate savings account | No debit card, funds stay protected |

Pro Tip: Set up automatic monthly transfers from your income account to your emergency reserve account. Automating this removes the decision entirely and keeps your safety net funded without effort.

What banking configurations do nomads actually use?

Most digital nomads use two to three banking relationships to cover 90% of their financial needs. The most effective structure follows a hub-and-spoke model.

The hub-and-spoke model explained

A hub-and-spoke approach works like this: your home-country bank is the hub. It receives income, holds savings, and handles any financial obligations back home such as taxes or loan payments. Multi-currency fintech accounts act as spokes. You fund them from the hub as needed, spend locally in whatever currency is required, and convert at favorable rates.

The numbered steps for building this structure are:

- Open a home-country hub account. Choose a bank in your country of tax residency. This account receives client payments, holds your emergency fund, and connects to your tax records. Keep the bulk of your savings here.

- Add a multi-currency fintech spoke account. These accounts hold multiple currencies simultaneously and convert at the mid-market rate. Fund this account from your hub before entering a new country.

- Open a local account for stays over three months. If you plan to stay in one country for a longer period, a local bank account simplifies rent payments, utility bills, and any local subscriptions. It also reduces the appearance of constant international transfers.

- Apply soft switching to upgrade without disruption. Soft switching means opening a new account for better features or higher interest rates without closing your existing accounts. You test the new account with small transactions, confirm it works for your needs, and then gradually shift more activity to it. Your old account stays open as a backup.

Pro Tip: Before entering a new country, transfer two to four weeks of spending money into your fintech spoke account in the local currency. This protects you from exchange rate swings and card acceptance issues on arrival.

Nomads who want to add another layer of financial flexibility sometimes explore offshore account options as part of a broader multi-jurisdiction strategy. This is worth researching once your core hub-and-spoke structure is stable. Understanding cross-border payment security also helps you make informed choices about which fintech platforms to trust with your daily spending.

What practical tips help nomads manage multiple accounts securely?

Managing several accounts does not have to be complicated. A few consistent habits keep everything organized and secure.

- Carry cards in separate locations. Keep primary banking cards in separate physical locations during travel. One card stays in your wallet, another in your luggage or a hostel locker. If your wallet is stolen, you still have access to funds.

- Automate small transactions to prevent dormancy. Banks close inactive accounts. Set up a small automatic transfer or a recurring subscription payment on each account to keep it active. A $5 monthly charge on a backup account is worth paying to keep it open.

- Enable in-app notifications on every account. Real-time alerts for every transaction catch fraud immediately. They also give you a clear picture of spending across all accounts without logging into each one manually.

- Review fee structures every six months. Fintech platforms change their fee models regularly. An account that was free last year may now charge monthly fees or limit free ATM withdrawals. A quick review twice a year prevents surprise charges.

- Prepare a compliance statement. If your bank asks about international activity, a short written explanation of your work and travel pattern resolves most AML holds quickly. Keep this document updated and accessible.

Pro Tip: Use a password manager to store login credentials for every banking app. Losing access to a banking app in a foreign country because you forgot a password is a preventable problem.

Staying on top of your digital security matters as much as your account structure. A VPN for banking access adds another layer of protection when you connect from public networks abroad.

Key Takeaways

Digital nomads who use two to three accounts across a home-country hub, a multi-currency fintech account, and a local account cover nearly all their financial needs while cutting fees, protecting deposits, and staying funded even when one account is frozen.

| Point | Details |

|---|---|

| Multiple accounts reduce risk | A frozen or blocked account does not cut off all your funds when you have a backup. |

| FDIC coverage requires multiple banks | US deposits are insured up to $250,000 per bank, so larger savings need two or more institutions. |

| Hub-and-spoke is the proven structure | A home-country hub plus one or two fintech spokes covers income, savings, and daily spending. |

| Soft switching upgrades without disruption | Open new accounts for better rates or features without closing existing ones. |

| Separation improves budgeting | Keeping rent or emergency funds in a card-free account prevents accidental overspending. |

The real reason I think every nomad needs at least three accounts

After years of watching nomads manage their finances on the road, the pattern is clear: the ones who run into serious trouble almost always have a single-account setup. They treat banking as a solved problem until it stops working, usually at the worst possible moment.

The insight that most articles miss is that the hub-and-spoke model is not just about fees. It is about psychological clarity. When your emergency fund is in a separate account with no debit card, you stop thinking of it as spendable money. That mental separation changes how you make decisions under pressure.

The other thing nomads consistently underestimate is how quickly AML flags escalate. A login from Thailand followed by a transaction in Portugal three days later is enough to trigger a review at many traditional banks. Having an unrelated secondary account is not paranoia. It is the same logic as carrying a backup passport photo. You hope you never need it, and you are very glad you have it when you do.

My honest recommendation: build your structure before you need it. Opening a backup account while your primary account is frozen is nearly impossible. Set up your hub-and-spoke system during a stable period, fund each account with a small amount, and test every card in a real transaction before you rely on it.

— Jay

Plan your finances with free tools from ToolsForExpats

Managing multiple bank accounts works best when you know exactly how much you need in each one. That starts with understanding your real cost of living in each destination.

ToolsForExpats offers a free suite of calculators built specifically for nomads and expats. Use the cost of living comparison tool to see how your budget changes between countries, or run the nomad cost calculator to estimate monthly expenses by city. Every tool is free, requires no account, and gives you the numbers you need to fund your accounts correctly. Visit ToolsForExpats to get started.

FAQ

Why do digital nomads use multiple bank accounts?

Digital nomads use multiple accounts to avoid account freezes, reduce foreign transaction fees, and protect deposits across institutions. A single bank rarely handles income receipt, multi-currency spending, and emergency reserves equally well.

How many bank accounts does a nomad actually need?

Most nomads need two to three accounts to cover 90% of their financial needs. A home-country hub plus one multi-currency fintech account covers the basics, with a local account added for longer stays.

What is soft switching in banking?

Soft switching means opening a new bank account for better features or higher interest rates without closing your existing accounts. It lets you test a new bank before committing to it fully.

Can a bank freeze my account because I travel internationally?

Yes. AML systems flag unusual international activity automatically, and accounts can be frozen without warning during a compliance review. A secondary account at a separate institution keeps you funded while the review is resolved.

How do I protect large savings as a nomad?

US deposits are insured up to $250,000 per bank per depositor under FDIC rules. Nomads with savings above that threshold need accounts at two or more FDIC-member banks to keep every dollar fully protected.