An offshore account is a foreign financial account held outside your country of tax residence, and digital nomads open them primarily to consolidate multi-currency income, reduce cross-border payment friction, and build a compliant financial structure that works across borders. The term "offshore" carries outdated connotations of secrecy, but the modern reality is far more practical. For nomads earning in USD, spending in euros, and living in Southeast Asia, an offshore account functions as a financial hub that holds multiple currencies without forcing constant conversions. Understanding why expats use offshore accounts starts with recognizing that global transparency frameworks like FBAR, FATCA, and the OECD Common Reporting Standard (CRS) have fundamentally changed how these accounts operate and who benefits from them.

Why nomads open offshore accounts: the core benefits

The primary reason digital nomads open offshore accounts is to manage money across borders without juggling a separate local account in every country they visit. That single advantage compounds into several concrete benefits.

- Multi-currency holding. You receive a client payment in USD, hold it in USD, and convert only what you need to euros for rent. No forced conversion at unfavorable rates.

- Reduced transfer fees. Routing money through an offshore account in a low-fee jurisdiction cuts the cost of international wire transfers compared to sending from a domestic retail bank.

- Income centralization. Clients in three countries can pay into one account. You stop chasing payments across platforms and currencies.

- Asset protection. Holding funds in a politically stable jurisdiction with strong banking regulations protects against currency devaluation in your current country of residence.

- Legitimate tax planning. Offshore accounts do not automatically reduce your tax bill, but they create the structure needed for compliant tax optimization strategies like foreign earned income exclusions or territorial tax planning.

Pro Tip: Open your offshore account before you leave your home country. Banks require address verification, and a stable home address makes the KYC process significantly faster than trying to open an account from a co-working space in Chiang Mai.

The offshore account advantages for nomads are most visible in cash flow management. You stop losing 2 to 3 percent on every currency conversion and start treating your finances as a single system rather than a collection of disconnected accounts.

How offshore banking interacts with tax reporting requirements

Tax reporting is the part of offshore banking most nomads underestimate, and getting it wrong is expensive. The rules differ depending on your citizenship, not just your residency.

U.S. persons face two separate reporting obligations. The first is the FBAR (FinCEN Form 114), which requires filing if your aggregate foreign accounts exceed $10,000 at any point during the calendar year. The second is FATCA Form 8938, filed with your tax return, which applies at much higher thresholds.

| Reporting Requirement | Filing Threshold (Single Expat) | Threshold (Married Filing Jointly) | Penalty for Non-Compliance |

|---|---|---|---|

| FBAR (FinCEN 114) | $10,000 aggregate | $10,000 aggregate | Up to $16,536 per account (non-willful) |

| FATCA Form 8938 | $200,000 at year-end or $300,000 anytime | $400,000 at year-end or $600,000 anytime | Up to $50,000 per violation |

The FBAR threshold is low enough that almost any nomad with a funded offshore account will trigger it. That means filing is not optional. It means filing is the baseline expectation.

Beyond U.S. requirements, the OECD CRS automatically exchanges financial account information between participating countries, covering account holder identity, balances, and income. Over 100 countries participate. The era of anonymous offshore accounts ended with CRS. What replaced it is a system where your offshore bank reports your account details to your country of tax residence automatically, every year.

This shift changes the entire calculus of offshore banking. The goal is no longer to hide assets. The goal is to structure and report everything properly so your accounts function without interruption. Nomads who treat offshore accounts as a tax loophole face penalties. Nomads who treat them as a compliance tool benefit from them.

Pro Tip: Consult a cross-border tax specialist before opening an offshore account, not after. Resources like SmileTax provide FBAR and FATCA guidance specifically for Americans abroad, which saves you from costly surprises at tax time.

What practical banking strategies do digital nomads use?

The most effective nomad banking setup is a multi-layer banking architecture built around three tiers: a hub account, fintech spending accounts, and an offshore account for cash flow and foreign exchange management.

- Hub account in your home country or tax residence country. This is your anchor. It holds your primary tax documentation, receives salary or business income, and serves as the reference account for your tax filings. Banks like HSBC Expat or Citibank International offer accounts designed for this purpose.

- Fintech multi-currency accounts for daily spending. Platforms like Wise and Revolut handle day-to-day transactions across currencies with low conversion fees. These are your spending layer, not your savings layer.

- Offshore account for cash flow management and FX optimization. This tier holds larger balances, manages currency conversion timing, and acts as the receiving account for international client payments. Jurisdictions like Singapore, the Cayman Islands, and the Channel Islands are common choices for their regulatory stability.

- Local accounts where you spend extended time. If you spend three months in Portugal, a local Millennium BCP or Novo Banco account makes rent and utility payments easier without triggering unnecessary international transfer fees.

The KYC requirements for offshore accounts are the biggest practical hurdle. Banks require proof of address, tax residence documentation, source of funds evidence, and sometimes in-person verification. Nomads who move frequently face a real risk of account freezing if their declared address no longer matches their actual location. Keeping your tax residence documentation consistent with what your bank holds on file is not a bureaucratic formality. It is the difference between a functioning account and a frozen one.

Understanding your tax residency status before opening an offshore account is the single most important preparatory step you can take.

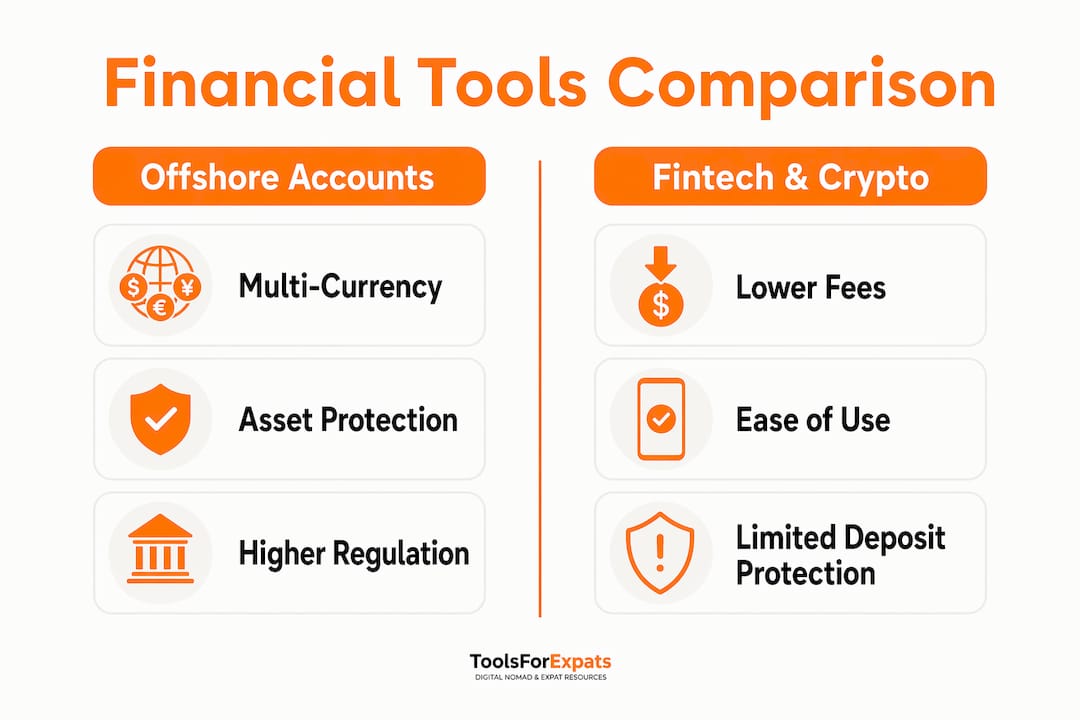

How do offshore accounts compare with fintech and crypto alternatives?

Offshore accounts are not the only option for managing money across borders, and they are not always the best tool for every job. The comparison below clarifies where each option excels.

| Feature | Offshore Bank Account | Fintech (Wise, Revolut) | Cryptocurrency |

|---|---|---|---|

| Regulatory oversight | High (FDIC equivalent, CRS reporting) | Medium (e-money license) | Low to none |

| Multi-currency support | Yes, with interest on deposits | Yes, with low conversion fees | Yes, but volatile |

| Account freeze risk | Medium (KYC/address issues) | Medium to high (compliance flags) | Low (self-custody) |

| FBAR/FATCA reportable | Yes | Yes (if qualifies as financial account) | Yes (if on exchange) |

| Setup complexity | High | Low | Medium |

| Best use case | Large balances, FX optimization | Daily spending, small transfers | Borderless payments, savings hedge |

Fintech platforms like Wise and Revolut solve the daily spending problem well. Their exchange rates are close to mid-market, and setup takes minutes. The tradeoff is that they are not banks. Your deposits are not insured the same way a regulated offshore bank account is, and their compliance teams are known to freeze accounts without warning when transaction patterns look unusual.

Crypto offers a borderless asset class that sidesteps jurisdictional restrictions entirely, but fiat on and off ramps still run through regulated exchanges tied to your tax home. Self-custody removes the geo-restriction problem but introduces its own risks around key management and volatility.

The practical answer for most nomads is not to choose one option but to use all three in the layered architecture described above. Offshore accounts handle large balances and FX timing. Fintech handles daily spending. Crypto handles specific use cases where traditional banking falls short.

- Offshore accounts are best for balances above $20,000 where deposit protection and interest matter.

- Fintech accounts are best for transactions under $5,000 where speed and low fees matter most.

- Crypto is best for payments to contractors in countries with poor banking infrastructure.

Key takeaways

Nomads open offshore accounts to build a compliant, multi-currency financial structure that reduces fees, protects assets, and supports legitimate tax planning across borders.

| Point | Details |

|---|---|

| Core purpose | Offshore accounts consolidate multi-currency income and reduce cross-border payment friction. |

| Compliance is mandatory | FBAR triggers at $10,000 aggregate; CRS reports your account to your tax residence country automatically. |

| Layered banking wins | Combine an offshore hub, fintech spending accounts, and local accounts for the most efficient setup. |

| Fintech is not a replacement | Wise and Revolut handle daily spending well but lack deposit protection for large balances. |

| Tax residency alignment | Your declared tax residence must match your bank's KYC records to avoid account freezes. |

The part most guides skip about offshore banking

I have spoken with dozens of nomads who opened offshore accounts expecting their tax bill to shrink automatically. It does not work that way, and I want to be direct about that. The actual benefit of offshore accounts is operational, not magical. You gain control over when and how you convert currencies, where large balances sit, and how your income flows across borders. That control has real financial value, but it requires planning and ongoing maintenance.

The mistake I see most often is nomads who open an account in a favorable jurisdiction, stop updating their address with the bank, and then discover their account is frozen six months later when they need it most. Banks classify you for CRS reporting based on your declared tax residence. If that declaration is stale or inconsistent, your account becomes a compliance problem for the bank, and they resolve that problem by freezing or closing your account.

My honest recommendation is to treat your offshore account like a business asset that requires annual review. Check that your tax residence documentation is current. Confirm your address on file matches your actual situation. Review whether the jurisdiction you chose still offers the regulatory stability and fee structure that made it attractive when you opened the account. Regulations change, and the account that made sense in 2023 may not be the right fit in 2026.

Maintaining a paperless financial life abroad makes this annual review far easier. Digital document management means your KYC files are always current and accessible, regardless of which country you are in when the bank asks for them.

— Ceyhun

Plan your finances with ToolsForExpats

Managing offshore accounts is one piece of a larger financial picture that includes living costs, currency decisions, and budget planning across countries.

ToolsForExpats offers a free suite of calculators and tools built specifically for digital nomads and expats. Use the nomad cost calculator to estimate your monthly expenses by city, which directly informs how much you need to hold in each currency. The cost of living comparison tool lets you weigh up destinations side by side so your banking structure matches your actual spending reality. Everything on ToolsForExpats is free and requires no account to access.

FAQ

Why do digital nomads open offshore accounts?

Digital nomads open offshore accounts to hold multiple currencies, reduce cross-border transfer fees, and centralize international income in a single compliant account. The core benefit is operational: one account that works across borders instead of a separate local account in every country.

Are offshore accounts legal for U.S. citizens?

Offshore accounts are fully legal for U.S. citizens, but they require mandatory reporting. U.S. persons must file an FBAR if foreign account balances exceed $10,000 in aggregate, and FATCA Form 8938 applies at higher thresholds for expats.

What is the difference between FBAR and FATCA?

FBAR (FinCEN 114) is filed separately from your tax return and triggers at $10,000 aggregate across all foreign accounts. FATCA Form 8938 is filed with your tax return and applies at $200,000 for single expats at year-end, with higher thresholds for married filers.

Can fintech apps like Wise replace an offshore bank account?

Wise and Revolut handle daily spending and small transfers efficiently, but they are not banks. They lack the deposit protection and large-balance stability that a regulated offshore bank account provides, making them a complement rather than a replacement.

What happens if I do not update my address with my offshore bank?

Banks use your declared tax residence to classify your account under CRS reporting rules. If your address is outdated or inconsistent with your actual tax residence, the bank may freeze or close your account to resolve its own compliance obligations.