A nomad emergency fund is a dedicated cash reserve that digital nomads and expats maintain to cover unexpected costs specific to a mobile lifestyle, from emergency flights to laptop replacements to sudden visa complications. Unlike a standard emergency fund, this reserve accounts for currency risk, variable income, and the reality that you may need funds instantly from the other side of the world. Financial experts recommend a minimum of 3–6 months of essential living expenses as a baseline, with 6–12 months advised for those with irregular income or frequent location changes. Programs like the Homes On Wheels Alliance Nomad Emergency Fund (eFund) have distributed over $100,000 to more than 300 nomads since 2019, which shows just how real and common these financial emergencies are.

What is a nomad emergency fund and what should it cover?

A travel emergency fund covers far more ground than a traditional savings buffer. Most people think of emergencies as medical bills or job loss. For nomads, the list is longer and more expensive.

The core categories your fund must address include:

- Medical emergencies abroad. Hospital visits, prescriptions, and evacuation costs can reach thousands of dollars in countries where you have no insurance coverage or where your policy has gaps.

- Emergency flights home. Last-minute international airfare regularly costs $1,500–$2,000 or more. This figure should sit in your fund as a dedicated budget line, separate from your monthly living expenses.

- Equipment replacement. Your laptop and phone are your income. Replacing both can cost $2,000 or more, and you cannot wait weeks for a warranty claim when a client deadline is tomorrow.

- Visa and legal costs. Overstay fines, visa rejections requiring rebooking, and immigration attorney fees are real expenses that catch nomads off guard.

- Vehicle repairs. For road-based nomads, a broken-down van or RV can mean both a housing and transportation crisis at the same time.

- Temporary accommodation. If your housing falls through suddenly, you need cash to cover a hotel or short-term rental while you sort out the next step.

Pro Tip: Keep your emergency fund in a completely separate account from your daily spending. Out of sight genuinely means out of mind, and that separation protects you from slowly draining the fund on non-emergencies.

The key distinction is that this fund covers your burn rate during a crisis, not your normal monthly budget. Think of it as a financial firewall, not a flexible savings account.

How to determine the right size for your emergency fund

Fund size depends on where you live, how you earn, and how often you move. A nomad living in Chiang Mai, Thailand has very different baseline costs than one based in Lisbon, Portugal or New York City. Fund sizes range from $2,500 in budget destinations to $12,000 or more in high-cost regions. That range reflects real differences in rent, healthcare, and daily expenses.

Beyond raw size, the composition of your fund matters just as much as the total amount. Storing everything in one currency in one bank is a single point of failure. Store funds across 2–3 banks with roughly 40–50% held in your home currency for stability, and distribute the rest across currencies relevant to where you spend most of your time.

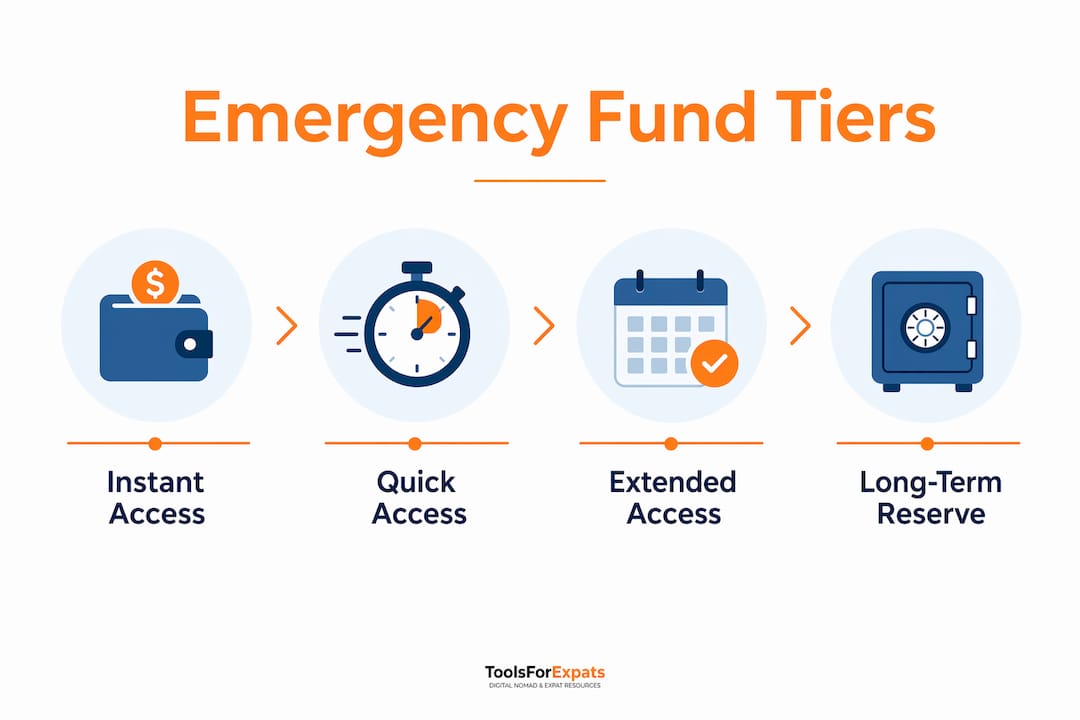

| Fund tier | Access speed | Recommended amount | Where to hold it |

|---|---|---|---|

| Tier 1: Instant access | Same day | 1 month of expenses | Checking account or Wise/Revolut |

| Tier 2: Short delay | 3–5 business days | 2–3 months of expenses | High-yield savings or secondary bank |

| Tier 3: Backup reserve | 1–2 weeks | Remaining months | Traditional bank in home country |

This layered liquidity approach means you always have something accessible, even if one account is frozen or a card is declined. Fintech tools like Wise and Revolut work well for Tier 1 because they support multiple currencies and instant transfers. Traditional banks anchor Tier 3 because they are more stable and less likely to freeze accounts without warning.

Pro Tip: Set your base currency allocation before you travel. Decide what percentage stays in USD, EUR, or GBP, and rebalance quarterly. Currency swings can quietly erode your fund's real value if you ignore them.

Reducing foreign exchange exposure also means checking rates on tools like digital currency guides before moving large sums between currencies.

How to keep your emergency fund accessible while traveling

Access is the most underestimated problem in nomad financial planning. Having money in an account means nothing if you cannot reach it when you need it.

The most common access failure is a 2FA lockout tied to an old SIM card. You swap your phone number when you move countries, and suddenly you cannot verify your identity to log into your bank. This locks you out of your own emergency fund at the worst possible moment.

Follow these steps to protect your access:

- Switch to app-based 2FA. Use Google Authenticator or Authy instead of SMS verification for every financial account. These apps work without a phone signal or local SIM.

- Get a VOIP number. A Google Voice number or similar service gives you a stable, location-independent phone number for account verification.

- Carry cards on two networks. Hold at least one Visa and one Mastercard from different banks. If one network goes down or a card is blocked in a specific country, you have a backup.

- Test your access annually. Log into every account, attempt a small transfer, and confirm your 2FA method still works. Do this before a major trip, not during one.

- Keep your fund separate from spending accounts. A dedicated emergency account reduces the temptation to dip into it and makes it easier to track the balance accurately.

- Store backup card details securely. Use a password manager like 1Password or Bitwarden to store card numbers, bank contacts, and account details you can access offline.

The goal is that no single failure, whether a lost phone, a frozen account, or a network outage, cuts off your access entirely. Redundancy is the whole point.

How to build and grow your nomad emergency fund

Building your fund starts before you leave home. Arriving in your first destination with a full emergency reserve already in place removes an enormous amount of financial pressure from your first months abroad.

Treat saving as a fixed expense, not what is left over at the end of the month. The most reliable way to grow your fund is to automate a transfer to your emergency account on the same day you receive income. If you wait to see what is left, there is rarely anything left.

Practical steps to build your fund consistently:

- Set a minimum baseline before departing. Aim for at least one month of your expected living expenses saved before you go. This gives you breathing room while you establish income abroad.

- Direct windfalls to the fund first. Bonuses, client overpayments, and tax refunds go straight to the emergency reserve until you hit your target amount.

- Schedule monthly money reviews. Sit down once a month to check your fund balance against your current cost of living. If you have moved to a more expensive city, your fund target needs to increase too.

- Separate emergency savings from investment accounts. Nomads who keep emergency funds in stocks or crypto face a serious problem during market downturns. Your emergency fund must be liquid cash, not assets you need to sell at a loss.

- Combine income streams to stabilize cash flow. Freelancers with one client are one cancellation away from a crisis. Adding a second income stream, whether consulting, affiliate income, or digital products, smooths out the gaps.

- Use a cost of living calculator to set your target. Your fund size should reflect where you actually live, not a generic number. The ToolsForExpats nomad cost calculator lets you estimate expenses by city so your target stays accurate.

Treat your emergency fund as a living system that needs regular review, not a number you set once and forget. Exchange rates shift, your lifestyle changes, and your costs evolve. Your fund needs to keep pace with all of it.

Building a solid nomad income backup plan alongside your emergency fund creates a genuinely resilient financial foundation.

Key takeaways

A nomad emergency fund is a multi-currency, layered cash reserve sized to 6–12 months of essential expenses, kept liquid and accessible across multiple banks and card networks.

| Point | Details |

|---|---|

| Fund size target | Hold 6–12 months of essential expenses, ranging from $2,500 to $12,000+ depending on your destination. |

| Cover nomad-specific costs | Budget explicitly for emergency flights ($1,500–$2,000) and equipment replacement ($2,000) as separate line items. |

| Layer your liquidity | Split funds across Tier 1 (same-day), Tier 2 (3–5 days), and Tier 3 (backup) accounts for reliable access. |

| Protect account access | Use app-based 2FA, a VOIP number, and cards on both Visa and Mastercard networks to prevent lockouts. |

| Review and rebalance regularly | Adjust your fund target monthly as your location, income, and exchange rates change. |

The part most nomads get wrong about emergency funds

I have talked with a lot of nomads who technically have an emergency fund but have built it in a way that would fail them in an actual emergency. The money is there on paper. The access is not.

The most common mistake is treating the fund as a static number. You hit $10,000, you feel secure, and you stop thinking about it. But if you moved from Tbilisi to Barcelona, your monthly expenses may have doubled. That $10,000 now covers half the time it used to. The biggest misconception is viewing the fund as fixed rather than something that needs active management.

The second mistake is keeping the fund in the wrong place. I have seen nomads with their entire reserve in a single brokerage account because the interest rate looked good. Then a market dip hits exactly when they need the money, and they are either selling at a loss or waiting for a transfer that takes five business days. Emergency funds must be cash, full stop.

The mental shift that actually helps is thinking of your fund the way you think about travel gear. You want it light, reliable, and ready to go. You test your gear before a trip. You should test your fund access the same way. Log in, make a small transfer, confirm your 2FA works. Do it before you need to, not during a crisis at midnight in a country where you do not speak the language.

Building this fund is one of the most genuinely freeing things you can do as a nomad. When you know the money is there and you can reach it, you make better decisions. You take the right client, not the desperate one. You leave a bad situation instead of staying because you cannot afford not to.

— Jay

Plan your fund with free tools from ToolsForExpats

Knowing your target fund size starts with knowing your actual costs. ToolsForExpats offers a suite of free calculators built specifically for digital nomads and expats, with no account required.

Use the nomad cost of living calculator to estimate monthly expenses by city and set a fund target that reflects where you actually live. The moving abroad budget calculator helps you map one-time relocation costs so your emergency reserve stays separate from your setup budget. For a full overview of every free planning tool available, visit ToolsForExpats and start building a financial plan that actually fits your lifestyle.

FAQ

What is a nomad emergency fund?

A nomad emergency fund is a dedicated cash reserve that covers unexpected costs specific to a mobile lifestyle, including medical emergencies, emergency flights, and equipment replacement. Financial experts recommend holding 6–12 months of essential expenses for nomads with variable income.

How much should a digital nomad keep in an emergency fund?

Fund size ranges from $2,500 in low-cost destinations to $12,000 or more in expensive cities, based on your monthly essential expenses. Start with a 3-month baseline and build toward 6–12 months as your income stabilizes.

Should a nomad emergency fund include investment accounts?

No. Emergency funds kept in stocks or crypto become inaccessible or lose value during market downturns, exactly when you need them most. Keep the fund in liquid cash accounts only.

How do I avoid getting locked out of my emergency fund abroad?

Switch all financial accounts to app-based 2FA using tools like Google Authenticator or Authy, and use a VOIP number for account verification. Carry cards on both Visa and Mastercard networks from separate banks as a backup.

How often should I review my nomad emergency fund?

Review your fund monthly to account for changes in your location, living costs, and exchange rates. Treat it as a living system that adjusts with your lifestyle, not a fixed number you set once.