A tax home is the general area of your main place of business or employment, and it is the single most important concept determining whether nomads qualify for major U.S. tax benefits. The IRS defines this concept formally, and understanding why nomads establish tax home status is the first step toward legally reducing your tax bill. The Foreign Earned Income Exclusion (FEIE) caps at $132,900 in 2026, with housing benefits tied directly to your tax home status. Get this wrong, and you could owe taxes on income you thought was excluded.

Why nomads establish tax home: the IRS definition explained

The IRS defines your tax home as the general area of your regular or principal place of business, employment, or post of duty. This is not your mailing address, your parents' house, or the city where you grew up. The location where you regularly work determines your tax home, full stop.

This distinction matters because nomads often confuse tax home with domicile or legal residence. These are separate legal concepts.

- Tax home relates to where you work, not where you live personally.

- Domicile is your permanent legal home, the place you intend to return to.

- Abode is where your personal, economic, and family ties are centered.

- Residence is simply where you physically live at a given time.

The IRS treats these four concepts independently. You can have a foreign tax home while your domicile remains in the United States. However, if your abode stays in the U.S., the IRS can deny your FEIE claim even if you spent 330 days abroad. Physical presence alone is not enough.

A special category applies to nomads with no fixed workplace: the itinerant worker classification. If you lack a regular place of business and a permanent residence, the IRS may classify you as itinerant. Your tax home then shifts to wherever you currently work. This sounds flexible, but it creates real complications for travel expense deductions and audit defense.

What are the advantages of establishing a tax home for nomads?

Setting up a tax home abroad unlocks several concrete financial benefits that make the effort worthwhile.

Foreign Earned Income Exclusion (FEIE): The 2026 FEIE limit is $132,900. A nomad earning $100,000 in foreign-sourced income could exclude the entire amount from U.S. federal income tax, provided they meet both the tax home test and either the bona fide residence test or the 330-day physical presence test.

Foreign housing exclusion and deduction: The housing benefit allows you to exclude or deduct housing costs above a base amount. The deduction limit is 30% of the FEIE cap, which equals $39,870 in 2026. Rent, utilities, and certain other housing costs in your foreign tax home location count toward this benefit.

State tax relief: Establishing a foreign tax home and severing ties with your U.S. state of residence can eliminate state income tax obligations entirely. States like California and New York are aggressive about claiming residents, so a documented foreign tax home strengthens your case for non-residency.

Audit defense: A consistent, documented tax home gives you a clear position to defend if the IRS questions your returns. Nomads without a defined tax home face far greater scrutiny.

One critical limit: FEIE does not eliminate the 15.3% self-employment tax on net earnings. Even with a foreign tax home, self-employed nomads still owe this tax on their net income up to the Social Security wage base of $168,600 in 2026. Tax home status reduces income tax, not self-employment tax.

What challenges do nomads face when setting up a tax home?

Establishing a tax home is harder for nomads than for traditional expatriates. The nomadic lifestyle creates specific friction points with IRS rules.

-

Itinerant classification risk. Without a fixed foreign base, the IRS may classify you as itinerant. Itinerant workers often fail the "away from home" test, which eliminates travel expense deductions. This classification also complicates FEIE claims.

-

Maintaining U.S. ties. Keeping a U.S. home, even rented out, creates problems. Renting out a U.S. home while abroad risks losing the "duplication of expenses" principle required to maintain foreign tax home status on audit. The IRS looks at whether you are genuinely paying for two homes.

-

Proving a regular place of business. If you work from cafes in Bali one month and Lisbon the next, you have no single work location. The IRS needs to see a pattern of regular work activity in one area to recognize a foreign tax home.

-

Losing travel deductions. Nomads who cannot prove a fixed tax home cannot deduct travel expenses as "away from home" costs. This is a significant financial loss for frequent movers.

-

Recordkeeping complexity. Proving a foreign tax home requires years of organized documentation. Most nomads underestimate this burden until they face an audit.

Pro Tip: Start a dedicated folder, physical or digital, on day one of your nomadic life. Label it "Tax Home Evidence" and add every lease, utility bill, and work contract as you go. Retroactive recordkeeping is far harder and less convincing to the IRS.

What criteria and evidence can nomads use to establish a tax home?

The IRS weighs several factors when determining whether your foreign tax home claim is valid. Understanding these factors lets you build a stronger case from the start.

Key factors the IRS considers

- Duration and regularity of stay. Spending most of your working year in one country signals a genuine work base. Sporadic visits do not.

- Lease or rental agreement. A signed lease in a foreign country is one of the strongest pieces of evidence you can hold.

- Local financial ties. A foreign bank account, local phone number, and utility bills in your name all demonstrate genuine economic presence.

- Business contracts and client location. If your clients are based in the country where you claim a tax home, that alignment strengthens your position.

- Residency visa or permit. A residency visa or permit shows the foreign government also recognizes your presence as legitimate.

- Severing U.S. ties. Closing U.S. gym memberships, canceling U.S. subscriptions, and selling or renting out your U.S. home all support the claim that your life has genuinely moved abroad.

The abode concept is the most commonly misunderstood factor. Physical presence alone without severing personal, economic, and family ties often results in FEIE denial even after meeting the 330-day foreign presence test. Spending 330 days in Portugal while keeping your U.S. bank accounts, family home, and social memberships active is a weak tax home claim.

A useful way to think about strong versus weak claims:

| Evidence type | Strong claim | Weak claim |

|---|---|---|

| Housing | Signed 12-month lease abroad | Short-term Airbnb stays |

| Banking | Foreign bank account, local bills | U.S.-only accounts |

| Work pattern | Regular clients in one country | Clients scattered globally |

| U.S. ties | U.S. home sold or rented out | U.S. home maintained personally |

| Documentation | 7 years of organized records | Partial receipts, no travel log |

Pro Tip: If you work with a tax professional who specializes in expatriate taxes, ask them to review your abode status annually. Your situation changes every year, and a single overlooked U.S. tie can unravel an otherwise solid claim.

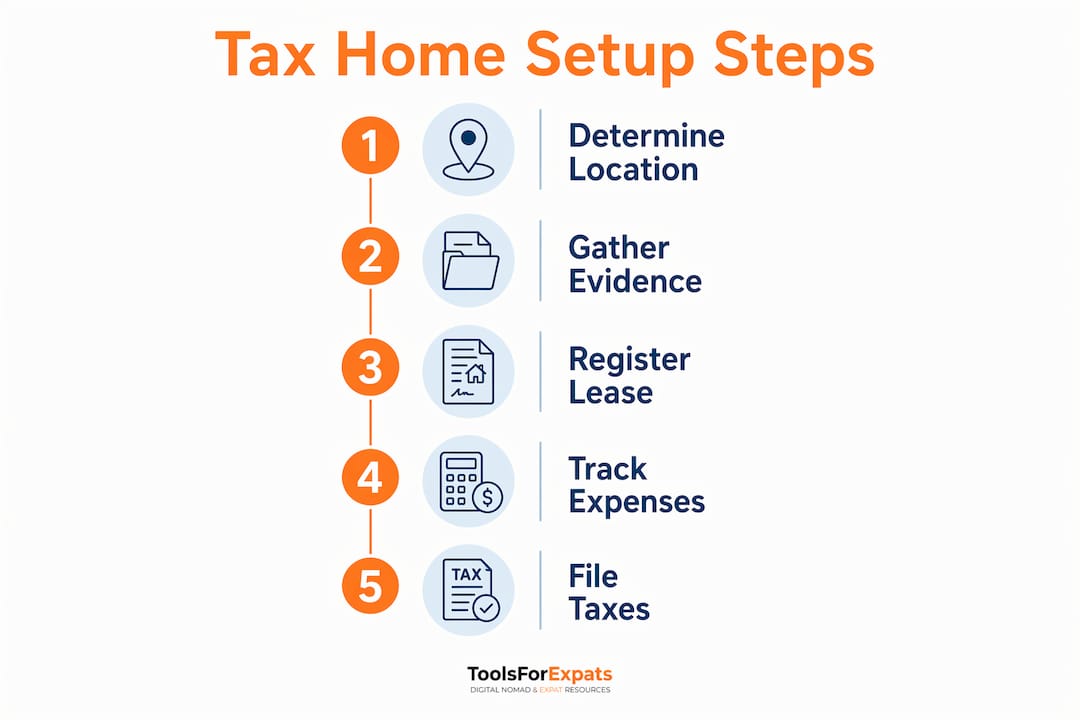

How can digital nomads practically set up their tax home in 2026?

Knowing the theory is one thing. Building a tax home that holds up under IRS scrutiny requires deliberate, consistent action.

- Establish a home base abroad. Rent an apartment for at least 12 months in your chosen country. A lease is your single strongest piece of evidence. If you plan to stay long-term, purchasing property is even stronger.

- Update your official documents. Change your driver's license, bank accounts, and professional registrations to reflect your foreign address. These updates signal a genuine shift in your life's center.

- Open a local bank account. A foreign bank account in your name, with regular deposits and local bill payments, demonstrates real economic ties to your tax home country.

- Track every move meticulously. Keep a travel log with entry and exit dates, countries visited, and purpose of each trip. The IRS can request this data going back years.

- Minimize U.S. ties actively. Cancel U.S. subscriptions, close U.S. storage units, and either sell or rent out your U.S. home. Each tie you sever strengthens your foreign tax home claim.

- Keep 7 years of records. Experts recommend 7 years of records for tax home proof, including lease receipts, utility bills, travel logs, and proof of local business activity. This surpasses the standard 3-year audit window and protects you in complex cases.

Nomads classified as itinerant can still qualify for FEIE. Itinerant status can shift your tax home to each foreign country you work in, provided all your work locations are foreign and your abode is not in the U.S. This is a viable path, but it requires even more rigorous documentation of each work location.

Pro Tip: Use a nomad expense tracker to log housing costs, utility payments, and work-related expenses by country. This data serves double duty: it supports your tax home claim and feeds directly into your FEIE housing deduction calculations.

Avoid the common digital nomad tax mistakes that cost nomads thousands each year. Many of those errors trace directly back to poorly documented or undefined tax home status.

Key Takeaways

Establishing a foreign tax home is the foundational requirement for nomads to access the FEIE, foreign housing benefits, and state tax relief, and it requires documented evidence of a genuine foreign work base with severed U.S. ties.

| Point | Details |

|---|---|

| Tax home is work-based | The IRS defines tax home by your work location, not your mailing address or family home. |

| FEIE requires tax home proof | The 2026 FEIE cap of $132,900 is only available to nomads who meet both the tax home test and a presence test. |

| Abode determines eligibility | Keeping strong U.S. personal and economic ties can disqualify your FEIE claim even after 330 days abroad. |

| Documentation is non-negotiable | Keep 7 years of leases, travel logs, and business records to defend your tax home claim under audit. |

| Self-employment tax still applies | FEIE reduces income tax but does not eliminate the 15.3% self-employment tax on net earnings. |

The part most nomads get wrong about tax home

Most nomads I've seen struggle with tax home status share one common mistake: they treat it as a paperwork problem rather than a lifestyle commitment. They file for FEIE, check the "foreign tax home" box, and assume the IRS will take their word for it.

The IRS does not take your word for it. The "duplication of expenses" principle is the real test. The agency wants to see that you are genuinely paying for a foreign home while also incurring costs to work away from it. If you are sleeping in hostels and working from cafes with no fixed base, that story does not hold up.

What I've found actually works is treating your tax home like a business asset. You invest in it deliberately: you sign a real lease, open a local bank account, and build a paper trail from day one. The nomads who get audited and win are the ones who can produce a chronological folder of evidence without scrambling.

The other thing worth saying plainly: meeting the 330-day test is necessary but not sufficient. I've seen nomads spend 330 days in Southeast Asia and still lose their FEIE claim because they kept a U.S. apartment "just in case." That apartment signals your abode is still in the U.S. The IRS reads that signal clearly.

Proactive recordkeeping and a genuine commitment to your foreign base are what separate a defensible tax home from a wishful one. Use specialized tools, consult a qualified tax professional who handles expatriate tax situations, and treat your tax home as seriously as you treat your income.

— Jay

ToolsForExpats tools for nomads planning their tax home

Planning a foreign tax home starts with knowing where you can afford to live, which visa you qualify for, and what your monthly costs will look like. ToolsForExpats gives you free tools to answer all three questions before you commit to a country.

The visa eligibility checker covers 20+ countries and shows you which digital nomad visas you qualify for based on your income and nationality. A valid visa or residency permit is one of the strongest pieces of evidence for a foreign tax home claim. The cost of living comparison tool lets you stack cities side by side so you can choose a base that fits your budget. You can also use the moving abroad budget calculator to plan your first year of expenses in detail. All tools are free and require no account.

FAQ

What is a tax home for a digital nomad?

A tax home is the general area of your main place of business or employment. For digital nomads, it is the foreign country or city where you regularly work and maintain your primary economic ties.

Can I qualify for FEIE without a fixed address abroad?

Yes, but it is harder. Nomads classified as itinerant can still qualify for FEIE if all their work locations are foreign and their abode is not in the U.S. Strong documentation of each foreign work location is required.

Does FEIE eliminate all U.S. taxes for nomads?

No. The FEIE excludes up to $132,900 of foreign earned income from federal income tax in 2026, but it does not eliminate the 15.3% self-employment tax on net earnings.

How long should I keep tax home records?

Keep at least 7 years of records, including leases, utility bills, travel logs, and business contracts. This exceeds the standard 3-year audit window and protects you in complex or extended IRS reviews.

Does renting out my U.S. home hurt my foreign tax home claim?

It can. Keeping a U.S. home, even as a rental, risks undermining the "duplication of expenses" principle the IRS uses to evaluate foreign tax home status on audit. Selling or fully renting it out with no personal use is a stronger position.